Microfinance was first implemented in India in the 1980s to empower women and reduce the intention of women empowerment and reducing poverty. The sector has problems with rural accessibility despite its promise. Microfinance companies provide banking services through channels other than traditional ones, bridging the financial gap for low-income and jobless people.

These days, it is an essential instrument for financial empowerment, especially for women, who are frequently regarded as trustworthy debtors. MFIs contribute to larger economic and social advancements by enhancing access to necessary resources like clean water and healthcare and offering social counsel.

Understanding of Microfinance Companies

Like banks, microfinance companies also offer credit, although microfinance loans—called microcredit—have lesser amounts. Usually, microentrepreneurs who require financial support to launch or expand their firms receive these loans. MFIs specifically serve this segment, unlike traditional banks, which frequently consider these clients too hazardous because they lack collateral and are involved in the unofficial economy.

MFIs evaluate the borrower’s willingness and capacity to repay before authorising a loan. To gather comprehensive information, this approach frequently includes conducting field surveys with the prospective entrepreneur’s friends. For minor loans, the requirements for acceptance are usually simple; however, larger loans could call for a track record of payback.

Developing a strong payment culture and providing financial literacy education are also crucial components of the process. A microfinance project’s success, as well as the entrepreneur’s, frequently hinges on the involvement of family members or close friends, who play a critical role in directly or indirectly supporting the business.

History of Microfinance Companies in India

Microfinance companies originated in the 19th century in India through informal lenders and moneylenders serving underprivileged populations. This pioneering effort paved the way for organised financial inclusion called microfinance companies.

Key Milestones of Microfinance Companies in India:

- 19th century: Irish Loan Fund system (Jonathan Swift)

- 1970s: Modern microfinance emerged

- 2006: Muhammad Yunus and Grameen Bank won the Nobel Peace Prize

Microfinance companies in India at present:

- Global microfinance institutions collaborate with the World Bank or operate independently

- Online platforms enable lenders to choose borrowers based on criteria like business type, location, or poverty level.

Microfinance companies empower low-income households through:

- Small microfinance loans

- Financial literacy

- Social guidance (For example., avoiding dowries, and accessing clean water)

Top 5 Microfinance Institutions in India

Here are the top 5 microfinance institutions in India:

Equitas Small Finance Bank

The lender provides small loans ranging from Rs. 2,000 to Rs. 35,000, specifically targeting individuals in the Economically Weaker Section (EWS) and Low Income Group categories within the country. These loans aim to support those with limited financial resources by offering accessible credit options.

| Loan Amount | Interest Rate | Processing Fee |

| Up to Rs. 25,000 | 24% p.a. | Nil |

| More than Rs. 25,000 | 23% p.a. | 1% + GST |

ESAF Microfinance and Investments (P) Ltd.

ESAF Microfinance provides support to over 400,000 members through its network of 150 branches. The organisation primarily aimed at uplifting economically and socially disadvantaged groups. To meet the diverse financial requirements of its customers, ESAF Microfinance offers a wide range of loan products, designed to cater to various needs and help members improve their livelihoods.

| Loan Amount | Rs. 50,000- 5 lakh |

| Interest Rate | At the discretion of the bank |

| Processing Fee | 1%-2% of loan amount + GST |

| Loan Tenure | 12 months- 35 months |

Fusion Microfinance Pvt Ltd.

Fusion Microfinance is a registered Non-Banking Financial Company-Microfinance Institution (NBFC-MFI) recognised by the Reserve Bank of India. It operates using the Joint Liability Group (JLG) lending model inspired by Grameen principles. In addition to delivering financial assistance and insurance coverage, Fusion Microfinance prioritises enhancing financial literacy among its customers.

| Loan Amount | Rs. 3,000- 60,000 |

| Loan Tenure | 8 months – 2 years |

| Interest Rate | 21%-21.50% p.a. As per reducing balance method |

| Processing Fee | 0 – 1% of loan amount + GST |

Annapurna Microfinance Pvt Ltd.

Annapurna Microfinance is dedicated to financially empowering marginalised communities through accessible loans and comprehensive support. Beyond lending, they foster entrepreneurship skills through technical training and financial education. As a leading NBFC-MFI in India ranked among the top ten in the industry, Annapurna Microfinance provides critical financial assistance, enhances economic resilience, and promotes self-sufficiency.

| Loan Amount | Rs. 1,500- 25 lakh |

| Loan Tenure | 12 months-240 months |

| Interest Rate | 18%- 28% p.a. (reducing) |

| Processing Fee | 1% – 2% + GST |

Arohan Financial Services Limited

1.9 million clients nationwide receive financial inclusion services from Arohan Financial Services Limited, the biggest NBFC MFI in Eastern India. In addition to financial products, Arohan offers non-financial services at accessible prices. Additionally, the organisation offers financing options designed specifically for Micro, Small, and Medium-Sized Businesses (MSMEs).

| Loan Amount | Rs.25,000 – Rs.1.5 lakh |

| Loan Tenure | 18 months – 24 months |

| Interest Rate | 24% – 26% p.a. |

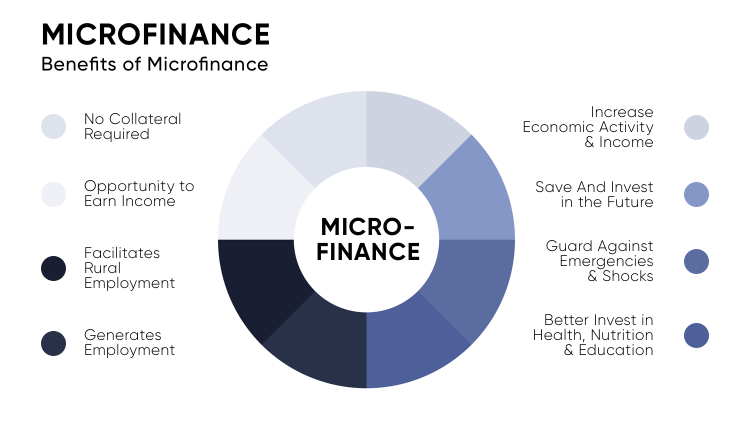

Benefits of Microfinance Institutions in India

Some of the benefits of microfinance companies are as follows:

Microfinance Companies Provide Immediate Funding

Microfinance companies play a key role in enhancing resilience within the broader economy. It helps households maximise their functioning, which boosts output and efficiency by offering financial support. Additionally, it guarantees constant access to vital resources by providing company owners with the capital they need to run and grow their enterprises.

Microfinance Companies Give Credit Access

Because larger banks typically avoid offering microfinance loans of lesser sums, access to credit is sometimes restricted for economically disadvantaged parts of society. Moreover, these establishments usually decline to lend money to borrowers who have little to no collateral. Additionally, many women lack proper identification documents or certificates proving ownership of land or property, which further complicates.

Microfinance Companies Provide Better Loan Repayment

Women have proven to be more reliable in loan repayment, leading microfinance companies to prioritise them as borrowers. This technique also contributes to the empowerment of women. Recognising this, microfinance organisations focus on women, achieving repayment rates exceeding 98%, despite the presence of overdue accounts at any given time. This approach underscores the role of women as safer investment choices in lending.

Cash Flow

Microfinance breaks the crippling connection between financial difficulties, subpar living conditions, and poor health by giving access to small loans and necessary resources, so upending the vicious cycle of poverty.

By bridging the financial gap, individuals can meet basic needs, improve sanitation, access clean water, and receive better healthcare, which boosts productivity and reduces chronic illness. This increases productivity and lowers the rate of chronic sickness.

Job Creation

Microfinance institutions spark local economic growth by enabling entrepreneurs to launch businesses and create jobs. This injection of employment opportunities stimulates the local economy, increasing money flow through nearby businesses and services, and fostering a vibrant economic environment.

Conclusion

Microfinance companies are indispensable in providing financial services to individuals who are typically excluded from conventional banking. These institutions help low-income individuals and entrepreneurs start or expand their businesses by giving them microcredit, or modest loans.

Unlike regular banks, microfinance companies focus on individuals working in the informal economy and borrowers without collateral. By evaluating the borrower’s willingness and capacity to repay, MFIs ensure financial support and encourage repayment discipline through financial literacy programs.